Hello and welcome back!

We’re back on track—yes, to Wednesday, as our name suggests.

For any economy today, Foreign Direct Investment (FDI) plays an important role in job creation, development of human capital, exports growth, and ultimately growth and development. In today’s competitive global landscape, even countries like the US are aggressively pressuring countries to channel investment into their own markets.

For Nepal, which has long struggled to realise FDIs, recent political developments and an outbreak of mob violence targeting private properties and large businesses have raised serious concerns—shifting the focus from feasibility and return on investment to the safety and security of investments themselves.

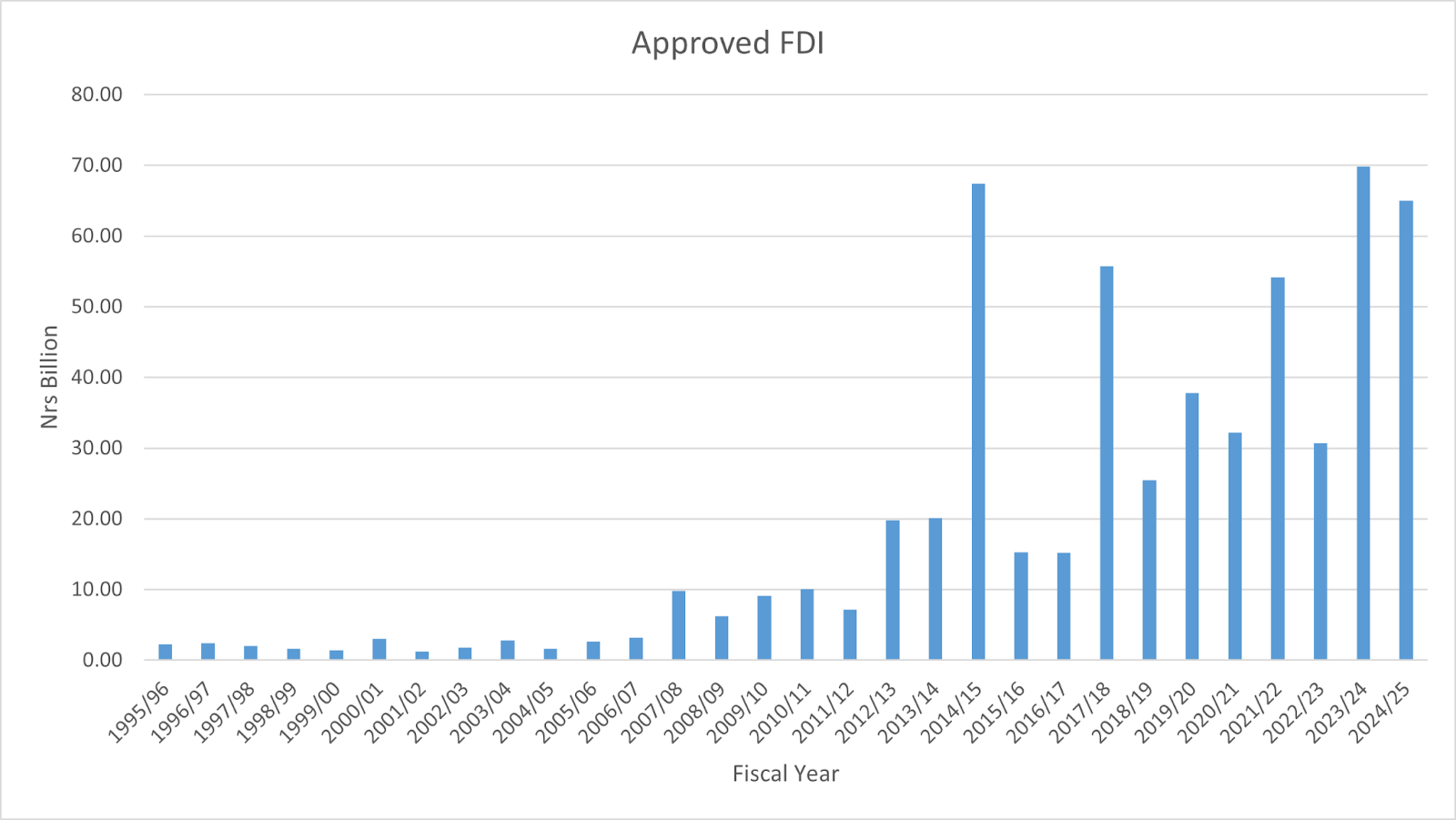

In this deep dive, we examine the trends of FDIs in Nepal, beginning with the fiscal year 2014/15, a pivotal period marked by a devastating earthquake that severely impacted the economy and subsequent adoption of a new constitution. A simple analysis of the FDI trend shows that though commitments remained high in between these periods, their conversion remained low, which has been on decline since 2020. For the last five years, the conversion-commitment ratio has been trending downwards from around 50% to around 20%. So what has happened in between these years?

While the new governments will now have to strive harder to rebuild the investors’ confidence following the recent events, it must equally reflect on the trials and tribulations of the past decade.

A systemic problem

For investors, developing economies offer opportunities for diversifying their portfolios, as such economies are associated with higher risks and potentially higher returns. As far as Nepal is concerned, the external costs for an investor are unfavourable socio-political climate as well as burdensome legal environment.

The approved FDI amount serves as a proxy for international interest in the Nepali market, while the actual inflows reflect the extent to which that interest is materialised. In certain fiscal years, as clearly visible in the chart, the discrepancy between approved FDI and conversion is staggering.

Another important consideration is that while conversion doesn't practically happen in the same approved year, there is a consistent pattern with actual inflows remaining below NRs 20 billion, even when commitments have exceeded NRs 60 billion at times. Over the decade examined in this deep dive, only around 29% of the committed amount has materialised. It shows that it is not just a matter of timing but a systemic problem. A deeper look into why some of these years stand out might give us insights into the deeper systemic problems.

Beyond the numbers though, the phenomenon also signals that even with multiple failures of conversion, interest in the Nepali market persists. Some fiscal years over the 10-year period illustrate this—they have some of the highest commitments perhaps as a reflection of optimism towards the environment for investment and a reaction to government actions to improve the business sector.

Unpacking the decade

The fiscal year 2014/15 witnessed one of the largest observed gaps in commitment and conversion since Nepal began trade liberalisation in the 1990s. Notably, around 80% of the approvals were for just five projects in the energy sector (Upper Marsyangdi-A, West Seti, Arun-3, Upper Karnali, Tamakoshi-3). This surge of interest in Nepal’s energy sector was most likely driven by a series of bilateral agreements with India and China, which happened without much ground level feasibility studies. The geopolitical rivalry between the two neighbours also played a role in expediting these agreements.

As of 2025, only one of these projects, Upper Marsyangdi 3, is operational. Tamakoshi 3 is essentially abandoned due to the original investor pulling out in 2016 with no new bidders on the horizon. The rest of the three projects are under construction with no concrete completion timeline with the West Seti and Arun III project at risk of ballooning costs arising from problems inland acquisition and compensation costs, while transmission infrastructure difficulties. Meanwhile, Upper Karnali risks becoming financially unfeasible due to Bangladesh canceling the 500 MW export agreement (PSA) under its revised policies (Special Power Act).

The fiscal year 2017/18 saw a similar trend where massive investments were approved in the energy sector where six projects amounted to around two-thirds of the total approvals. The reason for high FDI interest was likely due to the first general election following the adoption of a new constitution after a prolonged period of political uncertainty. The first investment summit and talks about ‘one-window’ facilitation of industry likely contributed to attracting large infrastructure projects where China was the largest bidder.

The conversion gap was largely caused due to policy stalling regarding major hydropower projects like Budhi Gandaki and Upper Tamakoshi. Literature surrounding this topic cites political instability, bureaucratic inefficiencies, land acquisition disputes, protracted environmental and social impact assessments (EIA/SIA), technical-geographical challenges, financial constraints, and contractor performance issues that collectively contributed to prolonged timelines and cost overruns.

The year also stands out as a critical turning point in the frequency and magnitude of large-scale FDI commitments, highlighting the role of democratic processes in increasing foreign investment interest. This is perhaps the most significant driver of foreign investment as the period following 2017/18 has seen commitments amounting to NRs 370.9 billion in eight years that followed—significantly surpassing the NRs 206.1 committed during the preceding two and a half decades.

Other periods of stark gaps are the recent fiscal years, 2023/24 and 2024/25. Despite commitments exceeding NRs 70 billion in 2023/24, less than 15% materialised. Much of the approved FDI was again concentrated in large-scale hydropower and manufacturing, sectors that are capital-intensive and require long lead times for implementation. A similar trend can be observed in the last fiscal year. Reports highlight that despite optimistic approvals, investors withheld disbursement due to persisting policy uncertainty, tax-related disputes, and a weak business environment.

It is a critical reminder that Nepal’s systemic weaknesses in converting commitments have not been resolved despite repeated reforms and liberalisation efforts and international organisations have started defining these patterns as traits rather than circumstance.

Policies with weak enforcement

Since 2014/15, Nepal has hosted several investment summits—first in March 2017, second in March 2019 and third only a year ago in April 2024. In 2019, it introduced a new Foreign Investment and Technology Transfer Act (FITTA), which laid out several reforms—such as streamlining authority for approving investment applications, introducing a single-window service mechanism, and removing investment thresholds for certain sectors to broaden participation.

The Act also aimed to simplify repatriation procedures, improve dispute settlement provisions, and enhance legal certainty for foreign investors. These measures were intended to signal a more open investment climate and align domestic policies with international standards, even as implementation challenges persisted.

The problem with Nepal’s investment climate remains that while sectoral provisions exist on paper, their implementation remains shoddy leaving room for exploitation of the investor. While definite legal cases of corruption are lacking when it comes to FDI, there are several accounts from industrialists and investors charging the country’s political and bureaucratic leadership of extorting investors for facilitating investment.

Similarly, while the one window policy exists on paper, in reality unlike the name implies—a foreign investor looking to establish a project in Nepal must navigate a long and complex chain of approvals involving multiple agencies, each with its own procedures and timelines.

The process typically begins with submitting a proposal to the Department of Industry for project approval and foreign investment registration, followed by additional clearances from the NRB for foreign currency approval and repatriation guarantees. For large-scale projects, especially in infrastructure and energy, investors must then obtain survey or generation licenses from the Department of Electricity Development, secure environmental impact assessment (EIA) or initial environmental examination (IEE) clearance from the Ministry of Forests and Environment and get land acquisition permits from the Ministry of Land Management, Cooperatives and Poverty Alleviation.

Beyond these, they must also register the company at the Office of the Company Registrar, acquire industry-specific permits, and secure tax registration with the IRD.

In practice, each step involves lengthy documentation, frequent back-and-forth with officials, and often discretionary interpretation of legal provisions. Investors frequently report that the absence of a genuinely functional single-window mechanism forces them to deal with every agency individually, stretching approval timelines from what should be months to several years, ultimately discouraging timely capital deployment.

These were the primary reasons why Dangote Group, one of Africa’s largest multi-national corporations, which expressed interest in the Nepali cement industry around 2014 eventually exited. Being in between two economic powerhouses is a strategic position for large investors who can access big markets of India and China. Dangote thought the same.

What followed was a tale of one-sided effort with the group navigating all the legal, bureaucratic and political hurdles. So deeply was it interested in the project, they donated Rs 100 million to reconstruction and rescue efforts following the 2015 earthquake. Their tale of relentless efforts of trying to operate in the Nepali market for half a decade is well documented. It's a cautionary tale to any investor who dares think of Nepal as a good investment environment.

The exit came around 2018. Yet the challenges facing foreign investors persist. Nepal’s recent sovereign credit rating of ‘BB-’ with a stable outlook from Fitch offers both a mirror and a warning.

While the rating praised Nepal’s low external and central government debt, about 44% of GDP in FY 2023/24, well under the ‘BB-’ median of 55% and its strong external liquidity, robust foreign exchange reserves of over $13 billion, enough to cover nearly a year of external payments.

These are pieces of evidence that Nepal can build sound macroeconomic foundations when it commits to policy discipline. The rating had exceeded expectations and had ignited a political push towards further improving the investment environment. But with the recent destruction and a planned election, it is highly likely that some of these macro-indicators will take a hit further disincentivising investments, domestic or foreign.

The rating also underscores the very same structural weaknesses and governance gaps that perpetuate the discrepancy between approved FDI and actual inflows while creating a negative sentiment in investors—Fitch explicitly points to “burdensome procedures on profit repatriation,” “external transaction regulation,” and “frequent leadership changes” undermining long-term policy stability. These are not new critiques; they echo the same complaints found in domestic scholarship and media over a decade, meaning past reforms have either been shallow or poorly enforced.

A rising social dissonance

Figures and policies are only one part of the story in Nepal’s FDI problems. There is reason to believe that there lies a problem in the Nepali ethos that discourages foreign investment. This assertion becomes more apparent when we observe the dissonance between the country's investment environment and the collective reaction.

A simple matter of fact is that foreign investments are more heavily scrutinised than national projects. It is not an exaggeration to state that Ncell’s contributions revolutionised telecommunication in Nepal. Before Mero Mobile entered the telecommunications market, getting a sim card meant waiting in long queues, booking months in advance and filling up tiresome paperwork, which were replaced by easy-to-access and even free sim cards as part of their growth strategy.

After Mero Mobile was acquired by TeliaSonera and rebranded as Ncell, it introduced a new wave of technological innovation— expanded coverage, 3G speeds, and improved connectivity and quality which wouldn't have been possible with Nepali capital at that period. Over the course of the following decades, it displayed how competition in a monopolised market makes the consumers better-off and makes competitors more efficient.

Yet, despite its undeniable contributions, Ncell has often found itself in a rough spot—not because of market rejection, but because of the political and regulatory climate it operated in. Not that Ncell’s conduct has not been dubious, but over the years, the company became an easy target for political posturing and regulatory overreach. Regulatory bottlenecks, delayed approvals, and sudden changes in policy created an environment of uncertainty, often painting the investor as a villain rather than a partner.

Today, arson attacks on businesses like Hilton and the homegrown retail giant Bhatbhateni only add to this negative reputation. This pattern of expressing disapproval of foreign investments is a loud message to other potential investors: even if you build value in Nepal, shifting political winds and bureaucratic discretion can turn against you overnight.

And… what do you think?

Nepal’s FDI story isn’t just about money; it’s about trust. Investors hesitate not only because of red tape or regulations but because of a deeper uncertainty about how the state treats commitment, continuity, and accountability.

So, what do you think? Is Nepal’s hesitation toward foreign capital justified by past experiences, or are we letting fear and politics choke off opportunity?

Can we build an economy that welcomes investment without surrendering fairness and sovereignty?

That’s it for this week’s Wednesdays. We’re back and staying consistent. Wishes for Tihar and Chhath to those who celebrate and are celebrating this year.

Editor's Note: Farsight Impact produces Wednesdays under editorial guidelines and oversight of the_farsight.

Read More Stories

NEPSE falls nearly 75 points as market sentiment wavers

The stock market was unable to maintain the gains seen on Tuesday, slipping...

India has begun its long-delayed population census. Here's why it matters

India has begun the worlds largest national population count, which could reshape welfare...

The United Nations has called on Israel to repeal a law passed by...

Business + Finance + Economy + Tech + Environment + Nepal & South Asia + In-depth Analysis + News + Investigation + Research + Expert Opinion + Anatomy of Complex Issues.