Week in NEPSE: Dec 14-18

NEPSE index advanced with limited price movement.

The index opened at 2,607.05 on Sunday (Dec 14), growing higher mid-week, reaching an inter-week high of 2,632.81 on Wednesday (Dec 17), before declining to close at 2,615.03 on Thursday (Dec 18).

NEPSE price movement [Dec 14 - 18]

Similarly, market turnover softened at early sessions, dipping to NRs 3.29 billion on Tuesday (Dec 16), but gradually increased as the week progressed. Turnover peaked at NRs 4.58 billion on Thursday (Dec 18).

Index highlight

The recent week [Dec 14 -18] saw NEPSE edge higher, closing at 2,615.03, up by 0.78% from 2,594.87 on Sunday. While most of the main indices posted moderate gains, the sensitive float index led the week, with an increase of 1.23%, reflecting strength in freely traded large-cap shares.

Index performance (% change)

Among the sectors, the development bank and finance index led the gains with 2.5% and 1.52% respectively, followed by manufacturing and processing at 1.23% and banking index at 1.17%. Life insurance, hotel & tourism, and non-life insurance posted moderate gains. Meanwhile, hydropower, trading, investment, and mutual funds posted small gains, whereas other categories slightly declined by 0.17%.

Overall, the market displayed a gradual upward trend within a narrow momentum.

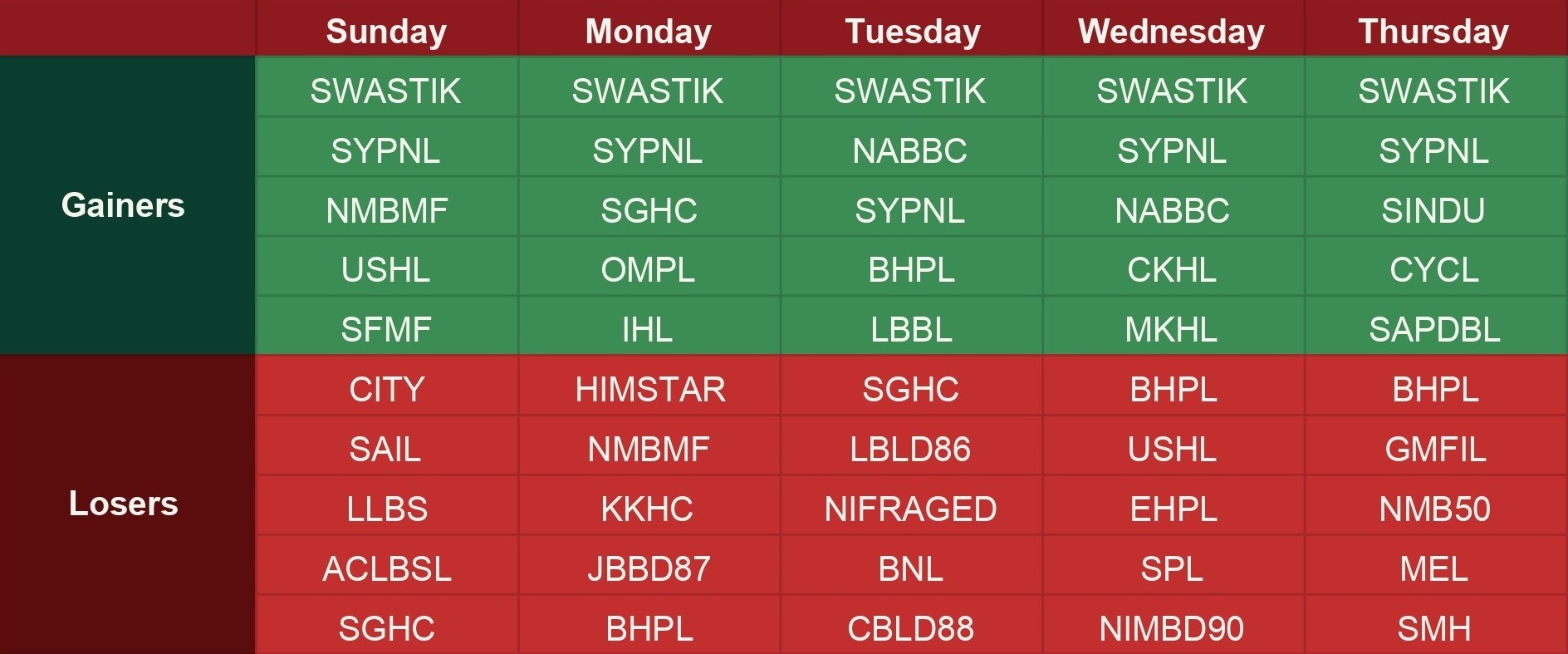

Stock in focus: gainers and losers

Swastik Laghubitta Bitiya Sanstha (SWASTIK) continues to dominate the gainers' list this week as well. SY Panel Nepal (SYPNL), a recently listed share, also maintained its growth streak from the previous week.

Other high-performing scripts, such as Narayani Development Bank (NABBC) and Sindhu Development Bank (SINDU), also contributed to this growing trend.

On the contrary, several stocks such as Barahi Hydropower (BHPL), City Hotel (CITY), and Himstar Energy (HIMSTAR) experienced a notable decline, marking a reversal in sentiment.

Market watch: News, policies, and listings

Inflation eases 1.11% in first four months, says NRB’s four-month data

Nepal’s inflation remained low at 1.11% in the first four months of FY 2025/26, primarily due to a 3.32% drop in food prices, easing pressure on household budgets.

Other macroeconomic updates from NRB show:

NRB updates banking rules on loans, assets, and governance guidelines

NRB has revised regulations on bad loan classification, non-banking assets, black listing, risk weighting, and shareholders' transactions of banks and financial institutions, including NIFRA.

Pari Passu Agreement: Pari Passu — Latin for ‘equal footing’, is used in finance where two or more parties (borrowers or lenders) share rights and obligations in equal proportion.

Interest Capitalized Reserve (ICR): Large projects under construction generally don't generate revenue, but borrowers are still required to pay interest on the loan. Instead of asking borrowers to pay interest during construction, banks add the unpaid interest to the loan amount. This process is called interest capitalization. Interest accrues, but banks don’t recognize it as profit immediately. For this, banks special reserve account to hold the interest income accrued on project loans during construction.

Loan-to-Value (LTV): ratio A financial metric that measures the percentage of an asset’s value (or purchase price) that is financed through a bank loan.

| Credit Rating | Risk Weight |

| AAA | 50% |

| AA+ - AA- | 70% |

| BB+ - BB- | 80% |

| BBB+ and below | 100% |

| unrated | 100% |

A study committee under SEBON proposes major changes to IPO eligibility

A study committee formed by SEBON in January this year has reportedly submitted its draft proposal to the board, suggesting amendments to current regulations on IPOs, rights issues, and lock-in period.

Under the proposal, hydropower companies will be permitted to raise capital from the public only after they enter commercial operations. For companies under the hotel and real estate sector, they would require a minimum paid-up capital of NRs one billion and at least three years of operational history to do so.

The proposed draft also increases the minimum IPO threshold, which currently sits at 10%. The companies will now have to either offer 20% of their issued capital or raise a minimum of NRs 300 million, whichever results in a larger public issue.

The draft has also revised the book-building mechanism, increasing the share allocation to institutional investors from 40% to 60% during the price-discovery stage. Regulators are seeking to address concerns that the existing framework gives a relatively small group of institutional investors disproportionate influence over IPO pricing, potentially disadvantaging retail investors. By raising the institutional allocation, the proposed changes aim to create a more robust and transparent price-discovery process while protecting broader market participation.

eSewa approves massive cash and stock dividend; Eyes IPO in near future

Amid a flurry of declarations of dividends this week by several listed companies, eSewa, the country’s prominent digital wallet platform, has approved an 80.53% cash dividend and 31.58% bonus shares.

During its 13th Annual General Meeting, the company confirmed the previously declared dividend distribution, authorising a cash payout of Rs 306 million (inclusive of tax), which accounts for 80.53% of the current paid-up capital. In addition, bonus shares worth Rs 120 million, representing 31.58% of the paid-up capital, will be issued from the company’s net profit and reserve funds.

eSewa also revealed plans to launch an initial public offering (IPO) in the near future.

Trading spotlight: IPOs and listed companies

Although there were no IPO listings on NEPSE this week. Bhujung Hydropower Limited has opened its IPO, offering 10,00,000 shares to project-affected locals in Lamjung and 1,00,000 shares to Nepali citizens abroad, which will run until January 1, 2026, and foreign subscriptions until December 22, 2025. The company’s total capital is NRs one billion, with 20% for the public. Kumari Capital manages the issue, while ICRA Nepal has downgraded the rating from B+ to B-. Bhujung, founded in 2015, is developing the 7.5 MW Upper Midim run-of-river project in Lamjung.

Read More Stories

NEPSE falls nearly 75 points as market sentiment wavers

The stock market was unable to maintain the gains seen on Tuesday, slipping...

India has begun its long-delayed population census. Here's why it matters

India has begun the worlds largest national population count, which could reshape welfare...

The United Nations has called on Israel to repeal a law passed by...

Business + Finance + Economy + Tech + Environment + Nepal & South Asia + In-depth Analysis + News + Investigation + Research + Expert Opinion + Anatomy of Complex Issues.