Bilateral Relations | Nepal-Mauritius DTAA | Agreement Termination | Taxation Policy

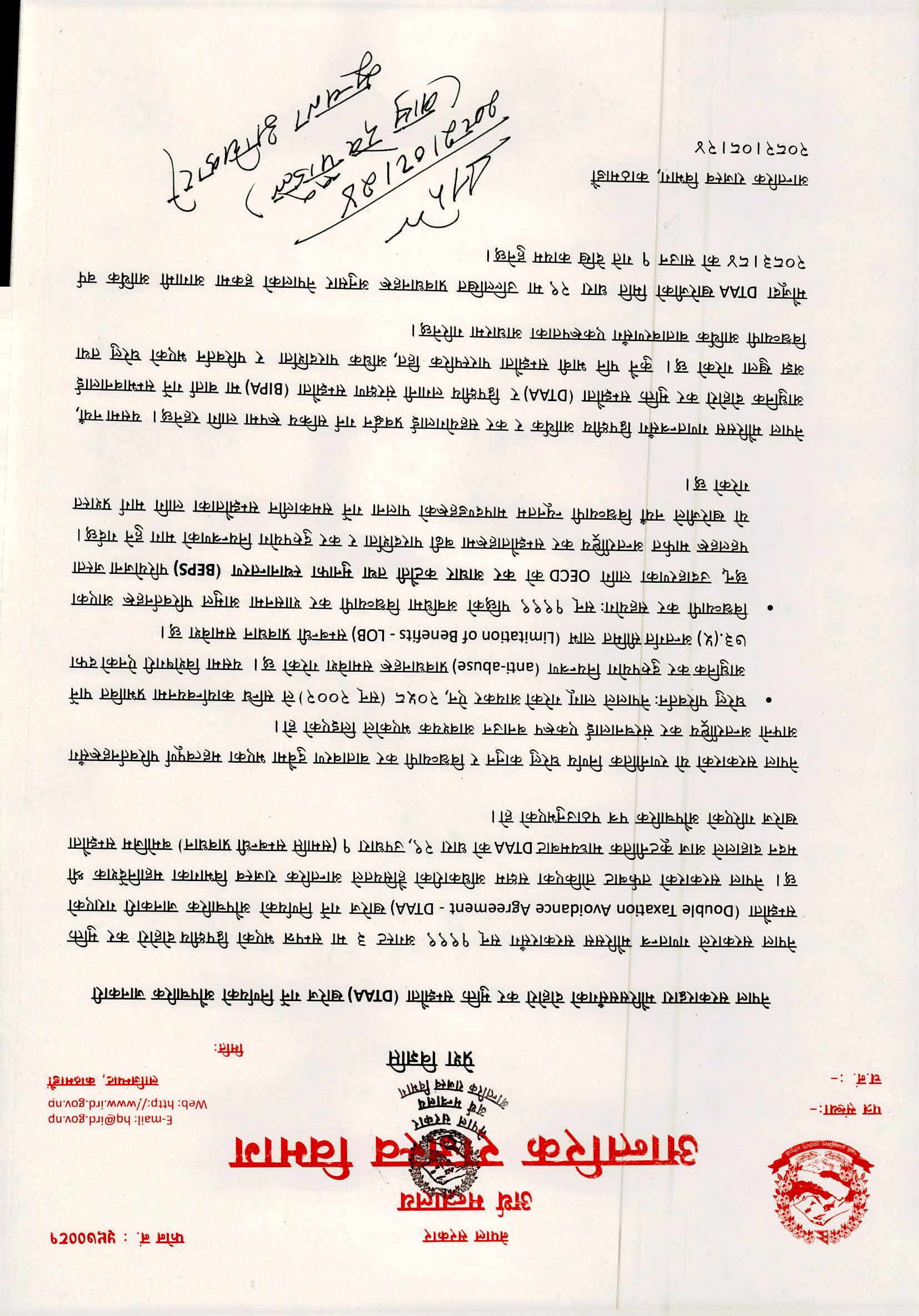

Nepal has formally notified Mauritius of its decision to terminate the bilateral Double Taxation Avoidance Agreement (DTAA) signed on August 3, 1999.

According to the Inland Revenue Department (IRD), Director General Madan Dahal sent the termination letter to Mauritius on December 10. The move was made under Article 29(1) of the DTAA.

A DTAA is a bilateral tax treaty between two countries designed to ensure that the same income is not taxed twice, once in the country where it is earned and again in the country where the taxpayer is based. These agreements typically define how various forms of income, including salaries, dividends, interest, royalties and capital gains, are to be taxed and allocated between the two jurisdictions.

Why was it terminated?

The treaty caught public attention recently with the government move to provide tax exemptions last month to Dolma Impact Fund under the DTAA treaty with Mauritius. Dolma is registered in Mauritius.

The government then decided to scrap the agreement with Mauritius.

In its press release, the IRD stated the decision follows Nepal’s efforts to align its tax structure with changes in its domestic laws and global tax conditions.

Nepal enacted its current Income Tax Act in 2002, three years after the agreement with Mauritius, introducing stronger anti-abuse measures that conflict with the DTAA’s provisions.

One of them is the Act’s Limitation of Benefits clause under Section 73(5), which basically prevents abuse of tax treaties by entities that are actually residents of the foreign country, and shell companies or entities created only to take unfair advantage of treaty benefits.

The IRD also explained that global tax governance has changed substantially since 1999. For instance, the introduction of the Organisation for Economic Cooperation and Development (OECD)’s Base Erosion and Profit Shifting (BEPS) project that requires the government to address tax avoidance through stronger measures.

One larger goal of the BEPS project is to ensure that profits are taxed where economic activities generating them take place and where value is created.

However, the government has expressed interest in pursuing future economic and tax cooperation with Mauritius, including the possibility of negotiating a new DTAA and a Bilateral Investment Protection Agreement (BIPA). Any new agreements would be based on mutual benefit and economic transparency, the IRD said.

The termination will take effect in Nepal from the next fiscal year.

For the avoidance of double taxation, Nepal’s Income Tax Act allows the government to sign international agreements with foreign countries.

After annulment with Mauritius, Nepal will still have DTAAs in force with 10 countries: India, China, Bangladesh, Pakistan, Sri Lanka, South Korea, Norway, Thailand, Qatar and Austria. Other countries vying for the agreement are the UK, Japan and the US, all of which are prominent sources of investments for Nepal.

Read More Stories

NEPSE falls nearly 75 points as market sentiment wavers

The stock market was unable to maintain the gains seen on Tuesday, slipping...

India has begun its long-delayed population census. Here's why it matters

India has begun the worlds largest national population count, which could reshape welfare...

The United Nations has called on Israel to repeal a law passed by...

Business + Finance + Economy + Tech + Environment + Nepal & South Asia + In-depth Analysis + News + Investigation + Research + Expert Opinion + Anatomy of Complex Issues.

{kind=link}