This week NEPSE began with a strong surge in the index, a market gain of 32.02 points in a single day to close at 2,672.55 on Sunday (Jan 18), as the date of the House of Representatives (HoR) election draws near.

The rise came as political parties fielded candidates and stepped up their campaign work. Trading volume reached 8.4 billion.

NEPSE price movement [Jan 18 - 22]

On the last trading day, the index bounced back again reaching 2,714.61, while trading volume stayed firm at 9.07 billion.

Index highlight

Alongside the main index, sensitive and float indices, which track strong and actively traded shares, also posted gains.

Index performance (% change)

Among sectoral indices, hotel and tourism emerged as the top performer, surging 2.69%. Hydropower followed closely with a 2.63% rise, while the development bank gained 2.38%. Manufacturing and processing also showed strength, climbing 2.29%, and the other index added 2.09%.

The investment index rose by 1.98%, while finance gained 1.65% and microfinance advanced 1.66%. Life insurance moved up by 1.53%, and non-life insurance posted a 1.59% increase. Banking, the market’s backbone, also closed higher with a 0.76% gain. The mutual fund index saw a modest rise of 0.34%. Trading was the only major index to close in the red, falling by 2.15%.

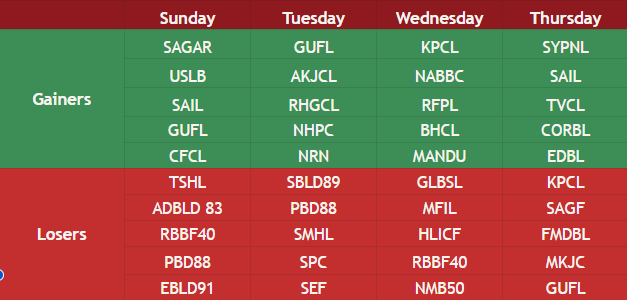

Stock in focus: gainers and losers

This week saw gains being spread across manufacturing, hydropower, development banks, and financial companies.

Stock gainers and losers

On the gainers' side, manufacturing and processing stocks such as Shreenagar Agrofarm Industries Limited (SAIL), Sagar Distillery (SAGAR), and SY Panel (SYPNL) drew strong buying interest.

Hydropower stocks showed mixed results. Stocks such as Mandu (MANDU), Kalika Power (KPCL), Ankhukhola (AKJCL), Rapti Hydropower and General Construction (RHGCL), and National (NHPC) were frequently listed among the week's gainers. At the same time, some stocks posted losses, such as Samling Power (SPC), Three Star Hydropower (TSHL), and Kalika Power (KPCL)

Similarly, financial institutions delivered a mixed performance this week. Stocks such as Gurkha Finance (GUFL), Corporate Development Bank (CORBL), Narayani Development Bank (NABBC), NRN Infrastructure and Development (NRN), and Unnati Sahakarya Laghubitta (USLB) drove the gains, while Gurans Laghubitta (GLBSL), Manjushree Finance (MFIL), and First Microfinance Laghubitta (FMDBL) lagged.

On the losing side, many debentures recorded a decline, including 10.35% Agricultural Bank Debenture 2083 (ADBLD83), RBB Focus 40 (RBBF40), 7.25% SBL Debenture 2091 (SBLD2091), and 10% Prime Debenture 2088 (PBB88).

While mutual funds such as Sanima Growth Fund (SAGF) and Siddhartha Equity Fund (SEF) also recorded a decline.

Market watch: News policies, and listing

NEPSE six-month snapshot: Early decline and gradual recovery

In the first half of 2025/26, the total NEPSE transaction amounted to NRs 7.21 trillion, a decline by 35.54% compared to six months of 2024/25.

The index saw decline since market resumed after September’s protest. October saw the steepest decline, with the index dropping 7% to 2,487.18. A prominent investor then said, “The market's future outlook is tied to macro factors: lower interest rates and excess liquidity favour a rebound. If political stability improves under the current interim and new government, a V-shaped recovery is possible.”

![NEPSE price movement [first six months]](https://farsightnepal.com/media/photos/chart_4.png)

The market began recovering in November, up 2.1% from October. By mid-January, NEPSE closed at 2,641.43, surpassing last year’s 2,594.13 for the same period.

Market capitalisation followed the same momentum. In September, the market declined to NRs 4,467.3 billion, before dropping further to NRs 4,157.90 billion in October, the lowest level in six months.

![Market capitalisation [first six months]](https://farsightnepal.com/media/photos/chart_3.png)

Market capitalisation followed the same momentum. In September, the market declined to NRs 4,467.3 billion, before dropping further to NRs 4,157.90 billion in October, the lowest level in six months.

The market recovered in November, rising to NRs 4,265.68 billion and continued the upward trend. By mid-January, the NEPSE index reached NRs 4,435.03 billion, surpassing last year's figure of NRs 4,302.88 billion in the same period.

475 projects pull 39.23 billion rupees FDI commitment in the first half of FY 2025/26

Foreign Direct Investment (FDI) commitment to Nepal reached NRs 39.23 billion across 475 projects in the first six months of FY 2082/83.

Among these, 314 projects worth NRs 2.81 billion were approved through the automatic route, while 161 projects totalling NRs 36.43 billion were approved through the approval route.

In terms of project scale, FDI commitment covered seven large industries, eight medium-scale industries, and 460 small industries. During mid-December to mid-January alone, 36 small-scale industries received NRs 599.5 million in commitment.

Sector-wise, agro and forestry industries attracted the highest investment, NRs 21.89 billion across 13 projects. Tourism followed with NRs 10.54 billion across 145 projects, services received NRs 3.46 billion for 31 projects, and manufacturing attracted NRs 2.03 billion for 27 projects. The ICT sector led in project numbers with 257 projects, but the total value was low at NRs 1.07 billion. Energy drew NRs 184.25 million for one project, and minerals received NRs 45 million for a single project.

Mid-year trade surges to NRs 1.1 trillion; India MoU streamlines cross-border clearance

In the first half of FY 2025/26, Nepal’s foreign trade reached NRs 1.1 trillion, a rise by 17.36% compared to the same period last year.

Nepal’s exports reached NRs 142 billion, a jump by 43.76%. Meanwhile, imports rose by 14.18%, just 61 million shy of reaching NRs 1,000 billion (currently at NRs 939.02 billion). The gap leaves the country with a trade deficit of nearly 800 billion.

Diesel led imports, with purchases from India worth NRs 58.28 billion. Refined soybean oil topped export, with shipment to India valued at NRs 56.08 billion.

The government also collected NRs 89.57 billion in import duties during the period.

Amid this rising trade volume, Nepal and India signed a Memorandum of Understanding (MoU) on the exchange of pre-arrival information on goods exported. As a standard global practice, the agreement allows both sides to share export data before goods reach the border.

Customs authorities will rely on data for risk analysis, faster clearance, and more targeted checks on high-risk goods. The information will be exchanged electronically and used only within limits set by national law.

The MoU was signed in New Delhi by Director General of Nepal’s Department of Customs Shyam Prasad Bhandari and Chairman of the Central Board of Indirect Taxes and Customs (CBIC) Vivek Chaturvedi.

Private producers get direct access to energy distribution

The Electricity Regulatory Commission (ERC) has approved the “Directive on Open Access in Electricity Transmission and Distribution System, 2025,” allowing private producers the right to sell power directly to buyers. The move marks a step toward a more competitive multi-buyer, multi-seller energy market.

Previously, Nepal Electricity Authority (NEA) acted as the single buyer of all electricity in the country. Private firms could generate power, but they had to sell it to NEA, which then distributed it onward.

Hydropower projects of at least five megawatts connected at 66 kV or higher, a captive power plant of at least one megawatt connected at 66 kV or higher, or a bulk consumer of five megawatts or more at 33 kV or higher to sell directly to industrial and commercial use. Licensed electricity traders and distributor companies can also participate. Private producers must supply at least ten megawatts for cross-border sales.

Currently, NEA acts as the nodal agency. It is required to process applications, assess plant capacity, grant approvals, and publish monthly reports on access points and durations.

Financial obligations include application fees ranging from NRs 5,000 to NRs 100,000, depending on the term and capacity. Users must also pay transmission and distribution operating charges, cross-subsidy surcharges, fixed-cost surcharges, and standby fees. Late payment incurs a 1.25% monthly fee.

The implementation will require a gradual rollout of additional procedures, rules, and directives. Under the new directive, the existing system has been revised, shifting responsibility to NEA to develop comprehensive implementation guidelines and standardised open-access agreements for use between license holders and consumers.

Read More Stories

NEPSE falls nearly 75 points as market sentiment wavers

The stock market was unable to maintain the gains seen on Tuesday, slipping...

India has begun its long-delayed population census. Here's why it matters

India has begun the worlds largest national population count, which could reshape welfare...

The United Nations has called on Israel to repeal a law passed by...

Business + Finance + Economy + Tech + Environment + Nepal & South Asia + In-depth Analysis + News + Investigation + Research + Expert Opinion + Anatomy of Complex Issues.