energy security | oil market | inflation | war | costs of war

After fears of a Middle East conflict sent crude prices toward $120, markets saw a sharp pullback to around $90, but the risk of prolonged supply disruptions could keep energy costs elevated worldwide.

After the Iran-US war, the world now faces the prospect of a sharp surge in oil prices, a development expected to strain inflation and growth across many economies in the coming months.

On Tuesday though, the oil prices fell sharply to around $90 after the crude nearly reached $120. The turnaround came after the US President Donal Trump's comment that the war would end ‘very soon’.

"If Iran does anything that stops the flow of Oil within the Strait of Hormuz, they will be hit by the United States of America TWENTY TIMES HARDER than they have been hit thus far," Trump wrote on social media.

The Islamic Revolutionary Guard Corps said that Iran's armed forces will "not allow the export of a single litre of oil from the region".

Despite this temporary pullback, prices have already hit significant highs, and market confidence in sustained downward momentum remains low.

Before the war started, the price was as low as $55 in December, with its $89 price point marking the highest it has been since October 2023 when it peaked above $90. In a recent interview with the Financial Times, Qatar’s Energy Minister Saad al-Kaabi warned that crude oil prices could soar to as high as $150.

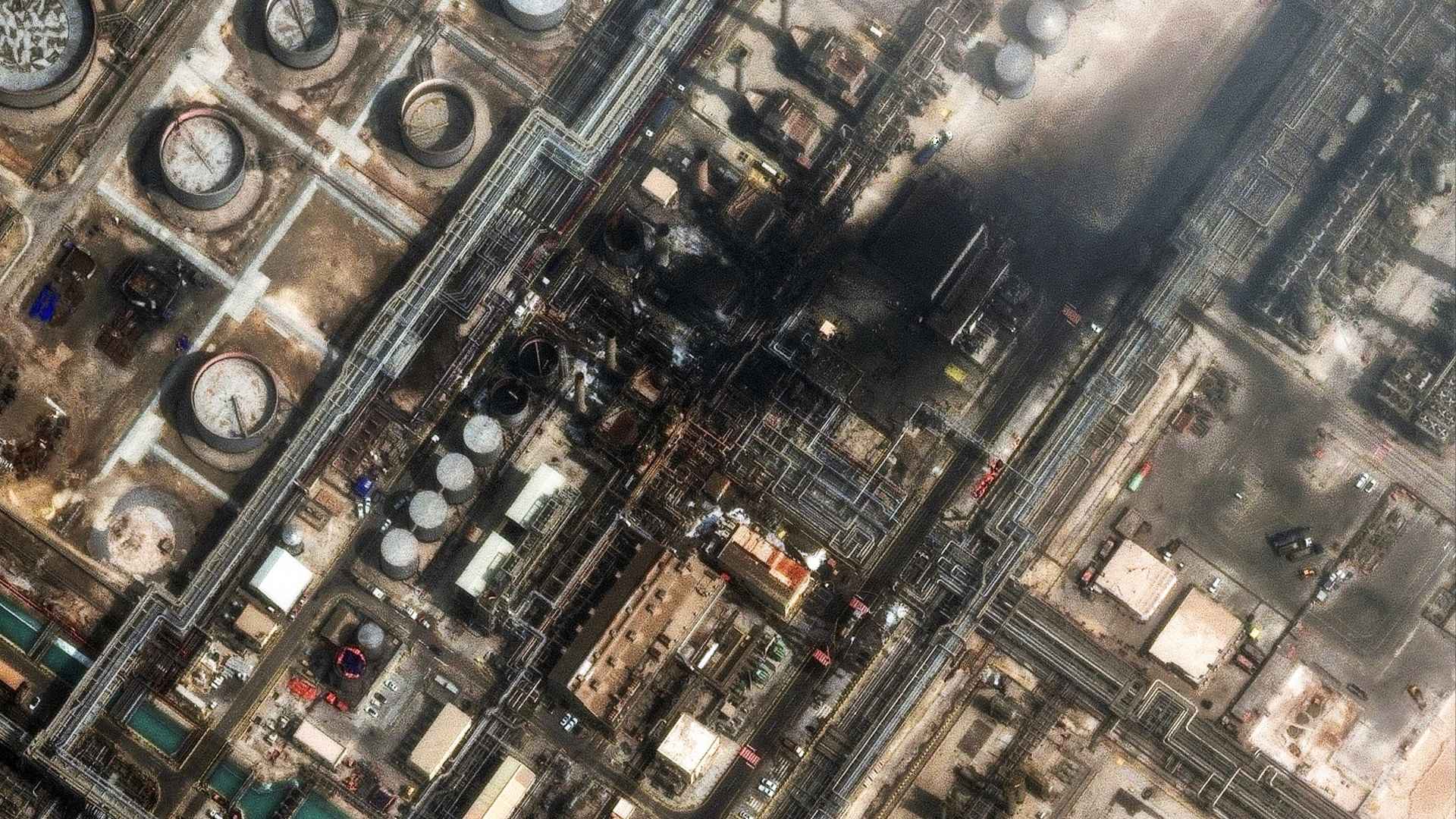

The surge is driven largely by concerns over potential long-term disruptions to energy supplies from the Middle East. Saudi Aramco, one of the world’s largest oil companies, on Tuesday warned of “catastrophic consequences” for oil markets if the Strait of Hormuz closure persists. Iran’s actions have partially choked this critical waterway, through which roughly 20% of global seaborne crude and substantial LNG shipments transit.

In addition to targeting the strait, Iran has also attacked oil refineries, further threatening production and adding pressure to global supply. Iran has conducted strikes on energy infrastructure across multiple Gulf oil producers, including attacks on Saudi Arabia’s Ras Tanura refinery and Bahrain’s Bapco oil complex, with debris from intercepted projectiles also reaching facilities in the UAE and hits near Kuwait and Qatar’s energy sites, intensifying fears of broader supply disruptions. Kuwait has already announced to implement a precautionary reduction in crude oil production and refining after the disruptions.

On Monday, Russian President Vladimir Putin expressed Russia’s willingness to supply oil and gas to Europe in response to soaring prices and supply disruptions. This comes despite the EU’s 2022 ban on Russian crude, as European countries have steadily cut their dependence on Russian energy to curb funding for Moscow’s war in Ukraine. Many analysts see this as a window for Russia.

For India, the stakes are particularly high. As one of the world’s most populous nations, it relies heavily on imports, nearly 90% of its crude oil, over 60% of its LPG, and more than half of its liquefied natural gas come primarily from the Gulf region. With soaring prices, India is likely to face severe consequences, and its markets have already reacted sharply to the disruption. Its rupee has fallen, supply is under strain, and the equity market has fallen. The geopolitical crisis could badly impact its inflation and fiscal balances as well as growth.

As such, it is under pressure to take all necessary measures. Earlier, the US Treasury reportedly issued a 30-day waiver allowing India to buy Russian oil currently stuck at sea, which Indian officials deny arguing that India doesn't need a third country’s decision. The reported US decision however came after continuous US pressure on India to stop buying oil from Russia. At the same time, domestic authorities are enforcing stringent measures to prevent hoarding and ensure the steady management of oil supplies.

South Korea plans to cap domestic fuel prices (first time in decades), expand a market stabilization fund, and diversify supply beyond the Strait of Hormuz.

Both Pakistan and Bangladesh have introduced fuel conservation measures after facing panic buying, and supply concerns. Pakistan has introduced a four‑day workweek, school closures, cuts to government fuel use, reduced spending, and fuel price hikes to manage limited reserves. Bangladesh has even secured extra fuel imports from alternative markets to avoid immediate shortages.

Meanwhile, on Monday, G7 finance ministers have discussed coordinated action on emergency oil stocks, including a possible release of strategic reserves to stabilize markets. The International Energy Agency (IEA) has urged its member states, the US, Canada, UK, Germany, France, Italy, Japan to maintain strategic oil reserves to consider releasing some of their stored oil into the market if supply disruptions or price spikes worsen.

“Energy security is of paramount importance to the global economy, and all parties bear responsibility for ensuring stable and uninterrupted energy supplies,” Chinese Foreign Ministry spokesperson Guo Jiakun said Monday when asked whether Beijing would join G7 discussions about a coordinated release of strategic petroleum reserves.

Read More Stories

NEPSE falls nearly 75 points as market sentiment wavers

The stock market was unable to maintain the gains seen on Tuesday, slipping...

India has begun its long-delayed population census. Here's why it matters

India has begun the worlds largest national population count, which could reshape welfare...

The United Nations has called on Israel to repeal a law passed by...

Business + Finance + Economy + Tech + Environment + Nepal & South Asia + In-depth Analysis + News + Investigation + Research + Expert Opinion + Anatomy of Complex Issues.